Tesla (TSLA) Q2 2024 Earnings Review (No Paywall)

By Yimin Xu. TSLA's fundamentals and technicals may never align. May they?

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Yimin Xu, July 26, 2024

10 Steps to understanding the Tesla (TSLA) Q2 Results

Today, we are going to review Tesla (TSLA)’s Q2 Earnings Report. We have LOTS of charts in this report.

One thing you should know about Tesla is that Elon does not like stock pickers, unless their surname rhymes with “ood”. According to Elon, people like Warren Buffet and me (why not) add no value to society. We just punch a bunch of numbers into a spreadsheet (Buffett probably does it in his head) and shuffle some capital around. In comparison, Elon is reshaping the humanity through electric cars, rockets to Mars, internet for the war zone, and viral memes on X.

Hats off to the guy, and I do recommend his latest biography by Walter Isaacson. Elon’s professional life is utterly fascinating and personal life perpetually turbulent.

But there might be another reason Elon doesn’t like stock pickers.

While Elon’s doing good for the humanity, his business does not come cheap. Any stock analyst who looks at Tesla, the CAR company, could easily conclude that it is very overvalued.

Elon does not like that. But anyone who dares short it gets burnt to dust.

Tesla, the AI, Robotaxi, and future car-insurance conglomerate, plays by the future visions and… price charts. TSLA all-in enthusiasts treat it as an option play for trillion dollar markets. And they seem to be right so far judging by the size of their wallets, though not the timeline of actual development.

Now, let’s analyse Tesla through a wide array of lenses to get an in-depth yet rounded view of the company fundamentals as well as the technical price action.

Before we begin, I have an exciting news to share!

I have launched my private channel at Cestrian to provide trade ideas in 3 key areas:

- Income Producing Instruments – including US Treasury ETFs, fixed income funds and Business Development Companies (BDCs)

- Equities – including mega-cap tech, financials (banks, asset managers, exchanges, payments companies)

- Crypto – selected crypto stocks and the underlying coins.

Today’s article is a good example of the depth and breadth we get into for each instrument. You can claim your 7-day free all-access via my Launch Pass page now!

1. Tesla is not a car company. Is it?

Tesla makes the great majority of its money by selling cars. You read that right.

78% of Tesla’s revenue comes from automotive related activities. Energy generation & storage and Services split the remaining 22% fairly equally.

If we further zoom in, Tesla’s automotive revenues can break split into sales, regulatory credits, and leasing. But it’s mostly just about car sales.

In Q2, automotive sales declined by 9%. This was primarily due to lower average selling prices and decreased deliveries of Model 3 and Model Y.

The services revenue increased by 21% due to higher non-warranty maintenance services, used vehicle sales, insurance services, and paid Supercharging revenue. This does not come at a surprise given the off-the-chart spikes in motor vehicle insurances in the past year. The general surge in insurance was due to a whole list of issues across supply bottlenecks, labour cost increases, and even bad driving (too many new cars & drivers since COVID).

Finally, Energy generation and storage revenue doubled YoY due to increased deployments.

2. Are Tesla’s car production and deliveries plateauing?

Tesla’s best selling models are by far its Model 3 and Model Y, which encompass 94-5% of the total production and deliveries.

In Q2, Tesla produced fewer cars than both Q1 or the prior year Q2, to the tune of 14%. Non Model 3/Y car production did increase by 24%, but still sharing a very small percentage of the total.

In terms of deliveries, Tesla delivered fewer cars YoY, but more than Q1. The stock price rallied when Q2 delivery announcement came out in July.

Tesla’s production facilities are spread across California, Shanghai, Berlin, and Texas. Tesla is in the pilot production stage for its Tesla Semi in Nevada. Tesla’s number 1 priority is to increase manufacturing capacity and ramp production at the these Gigafactories.

3. Overall performance is not all bad

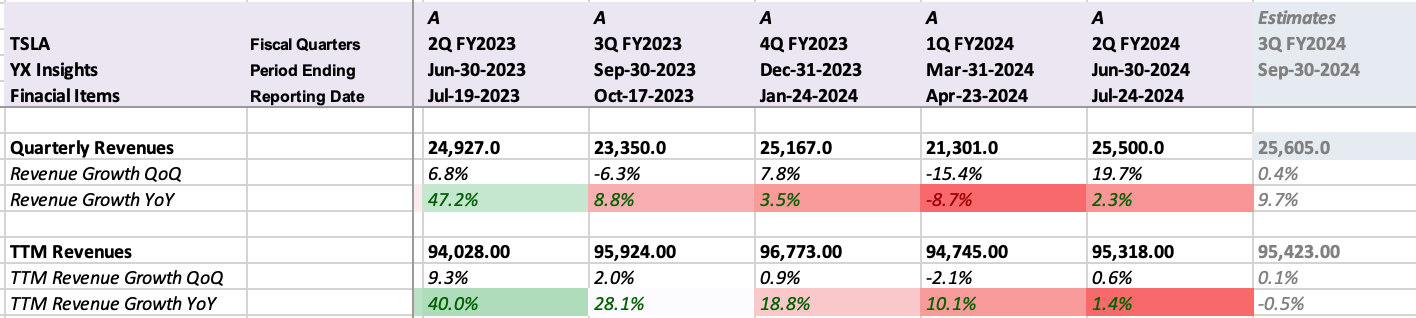

Tesla’s Q2 revenue is at least showing the right sign, growing 2.3% YoY - after a big Q1 quarterly decrease. In terms of the trailing-twelve-month revenue, we see that Tesla has braked to nearly 0 growth from the 40% growth a year ago.

The below chart reflects how much Tesla’s growth has been stalling since 2023.

Not everything is bad, however.

Gross margin is climbing back to 18%, while operating and EBITDA margins are growing from Q1. Tesla is also generating more free cash flows than both a year ago and Q1.

There has been a smaller CapEx spend this quarter than the past three quarters. Management guides total CapEx to exceed $10 billion in 2024, and $8-10 billion in 2025 and 2026. That’s basically on par with the current spend.

The stock-based compensation (SBC) is not huge either - about 2% of the total revenue. You wouldn’t tell by looking at Elon’s $56 billion compensation package. But the 2% is probably all him.

4. The stock tumbled post earnings

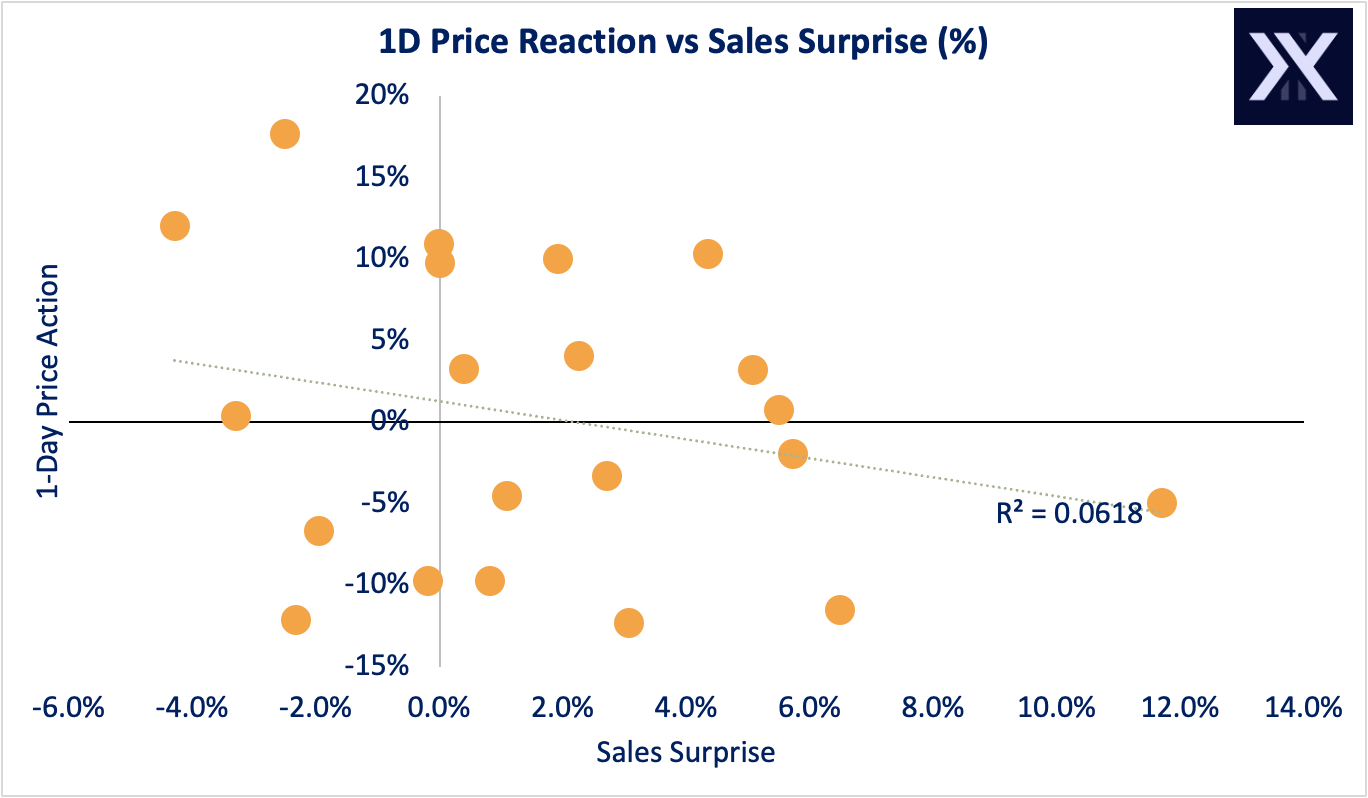

The stock fell by 12% after the earnings report, with the headlines citing Tesla’s EPS miss as the culprit. There could also have been a whole host of reasons, including the fundamental factors like the revenue slow down. Or that the stock ran up a lot between mid-June and mid-July and started to lose steam, so the earnings provided a sell-the-news event.

I wouldn’t get too fixated about the immediate market reaction. If you look at the 1-day price reaction versus Tesla’s historical sales surprise on ER, it would appear a random walk. Some days it goes up on good beats, and some days it goes down. The movements are likely more related to the chart technicals and the broader market conditions at the particular point in time than the actual headlines themselves.

5. The Robotaxi show is delayed, but Elon talks up Optimus

i) Robotaxi event moved to October 10th

The Robotaxi event has been moved from August to October, because Elon “wanted to make some important changes that would improve the vehicle.”

This may be an iPhone moment if successfully pulled off. At least, a lot of Tesla’s valuation hinges on it.

Cathie Wood believes that the (currently nonexistent) Robotaxi business will attribute to 90% of Tesla’s enterprise value by 2029. It will command a gross margin of 56% (vs. today’s 18%) and EBITDA margin of 32% (currently 14% not adding back SBC). The Robotaxi revenue will make Tesla a $2600 stock by 2029, or a market cap of $9 trillion.

A less bullish case: according to Straits Research, “The global robo taxi market… is projected to reach USD 107,682.14 million by 2031, registering a CAGR of 67.6% during the projected period (2023–2031).” This means even if it is a winner-takes-most market, Tesla can unlock just another $100billion extra revenue. At the 18 EV/ revenue multiple that Cathie uses, Robotaxi is worth an additional $1.8 trillion by 2031 (versus. today’s $680 billion total).

ii) “Optimus will exceed that of everything else that Tesla combined”

On the earnings call, Elon jumped at the opportunity to sell Optimus, the humanoid robot Tesla has been building. Elon points to a potential TAM of 20 billion units, which is basically from everybody on earth wanting one (“so it’s 8 billion right there”) and industrial uses (“at least as much, if not way more”).

Tesla should be in the pole position to take on this market, as it has both the best product and the manufacturing capability others don’t. Elon estimates Optimus should create “several times” Cathie Wood’s number on autonomous transport in market cap.

Another big dangling carrot right?

Bottom line: there is a lot of uncertainty but also opportunity in this space where estimates are largely finger-in-the-air.

6. Valuation has come down a lot, but maybe not enough?

On an absolute basis, an EV/ Revenue multiple of 7.2x for flat growth sounds pretty expensive, especially considering the low profit margins of a hardware company.

We already know this but please let me persist with the valuation talk until we get to the price charts.

If we examine Tesla’s historical performance, we see that multiples are already depressed compared with just 2 years ago, when the company revenue was growing at 70% (and EBITDA over 100%).

But you may spot that the valuation lines tend to sit above the TTM growth lines when the revenues & earnings accelerate. This is because the market is forward looking. When revenues & earnings decelerate, the valuation multiples sit below the growth line. With rate cut expectations and cooling inflation, the market is expecting an acceleration of growth for Tesla around the corner.

7. Tesla’s comparable valuation vs peers does not scream cheap

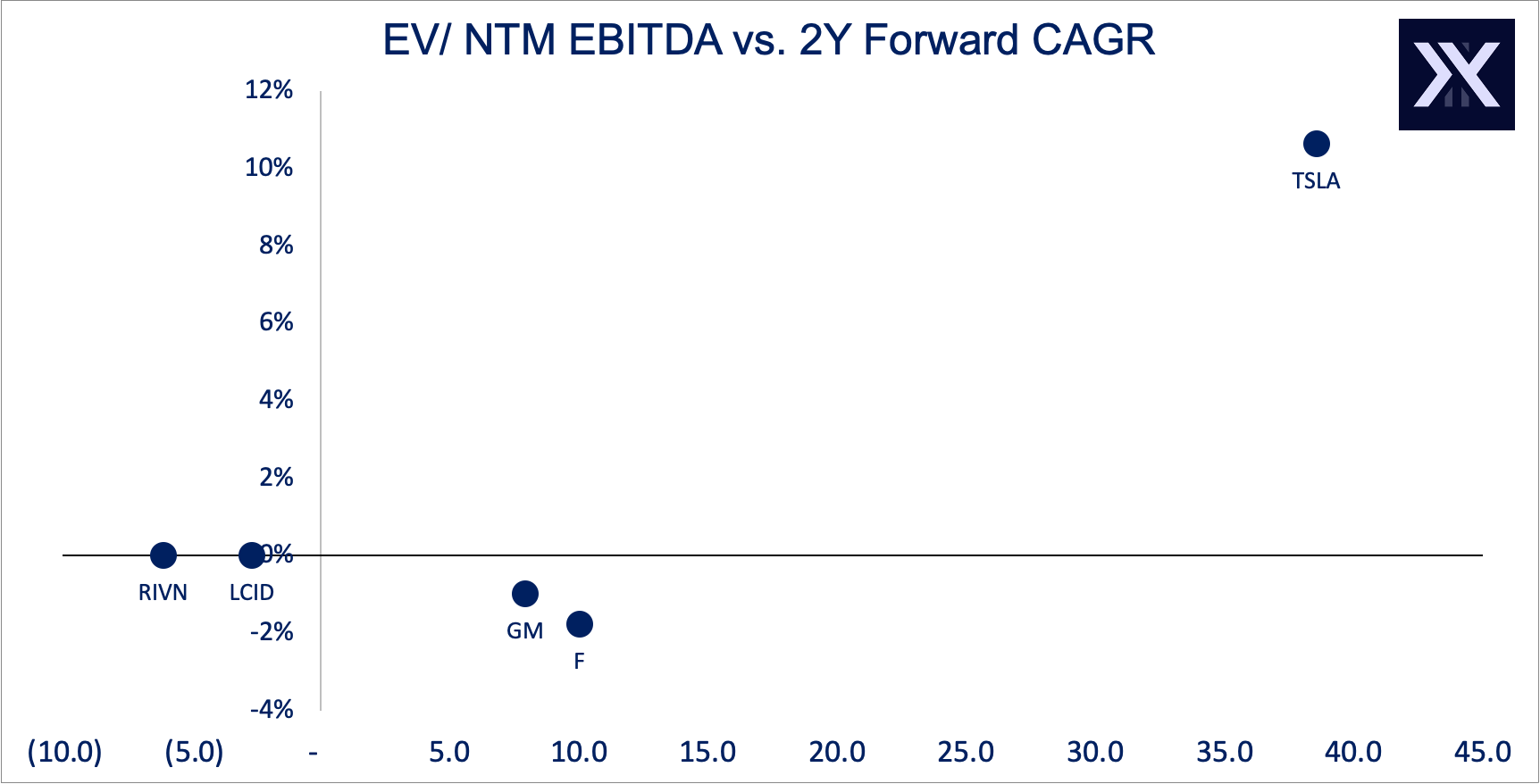

i) Auto peers

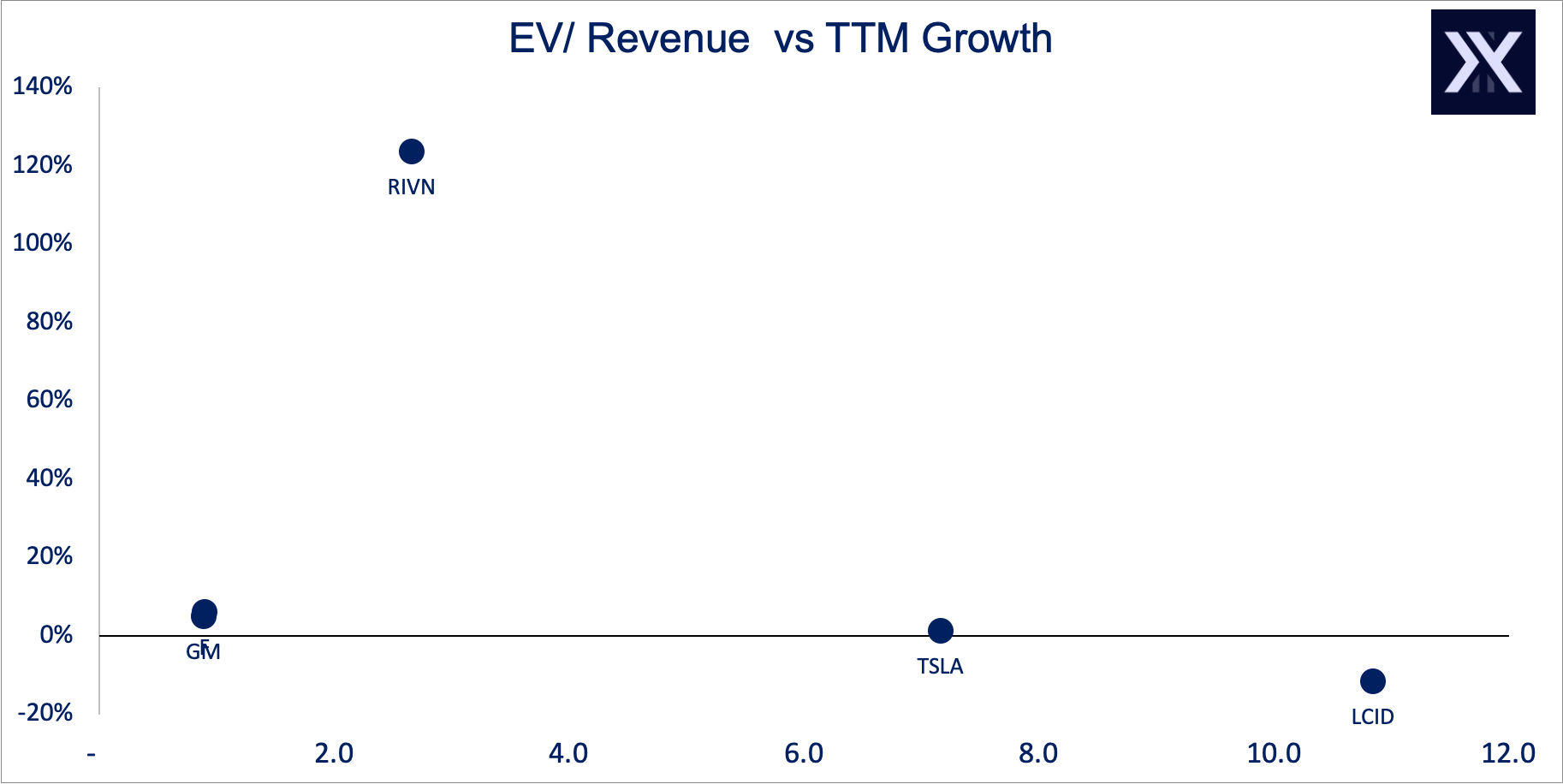

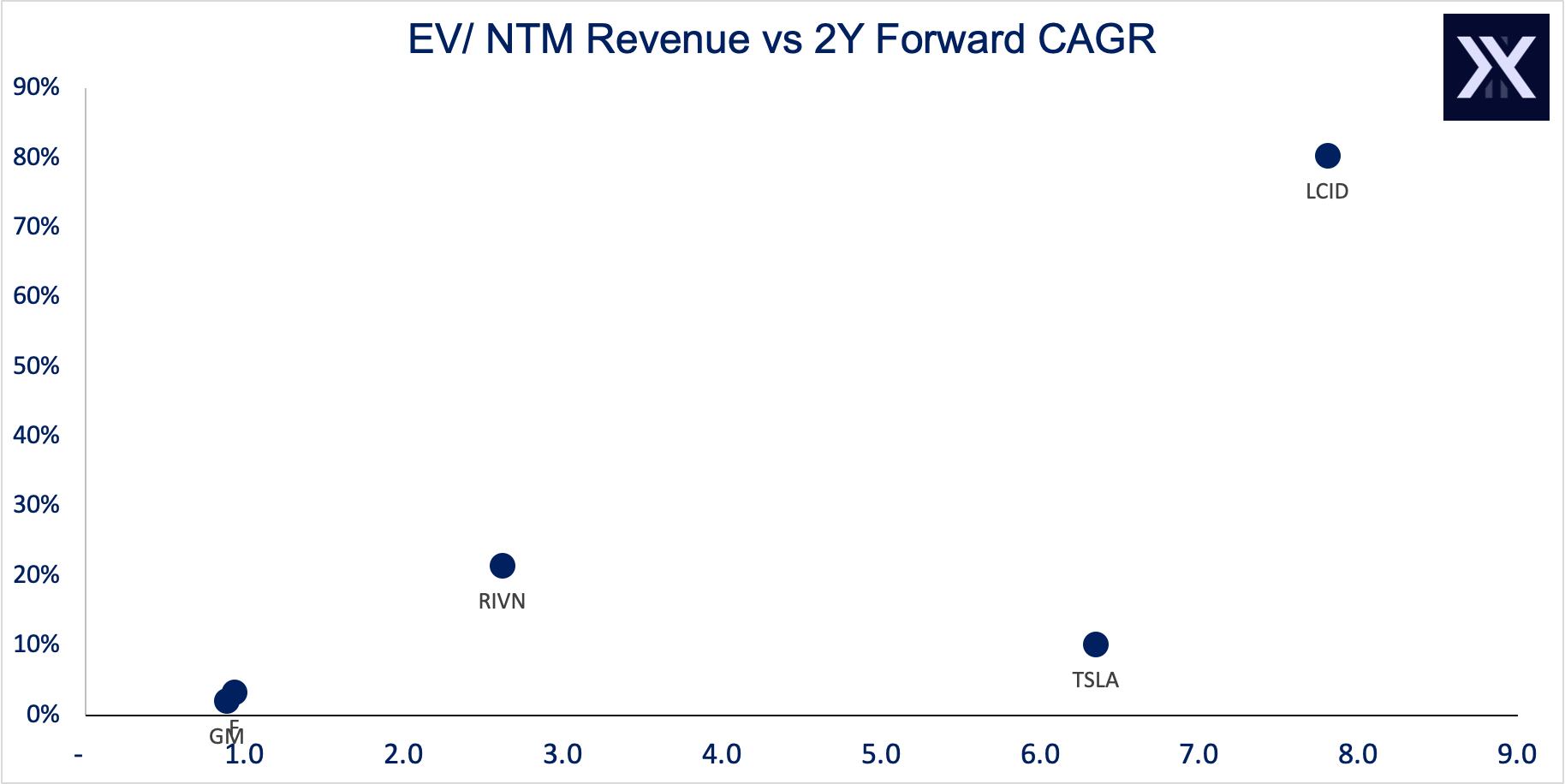

If Tesla is a car company, we could compare Tesla with its auto peers.

Ford and General Motors are sitting at the bottom left of this chart together, blended into a single dot. Both Tesla and Lucid appear expensive (little TTM growth but very far right on the x-axis for valuation multiples).

In terms of the forward-metrics, Lucid appears to be justified by its forward revenue growth projection. Tesla looks expensive still.

However, Tesla’s EBITDA growth seems to justify its valuation a little bit better.

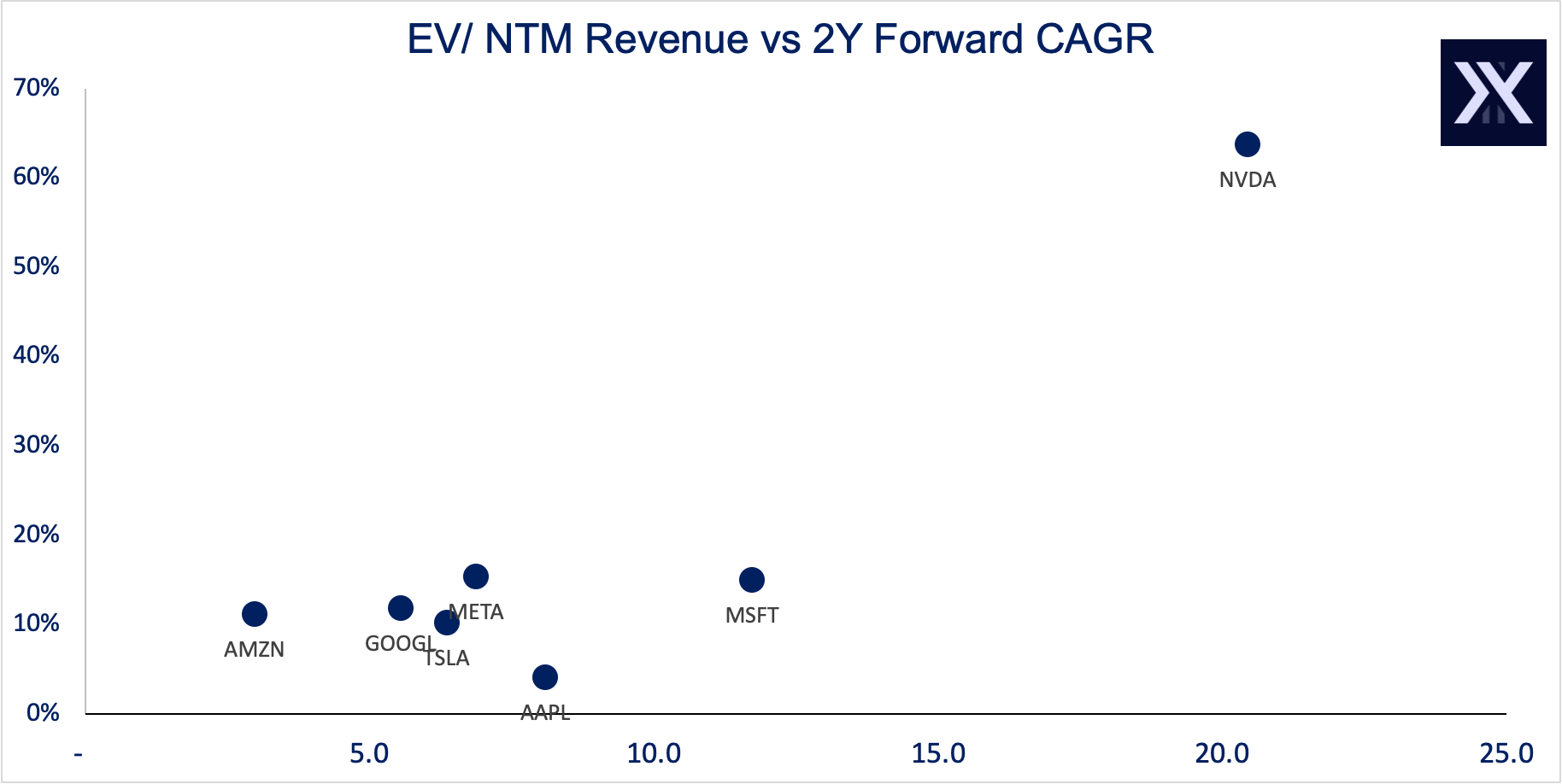

ii) Magnificent 7 peers

Tesla is clustered with AAPL on the little growth, high multiple side in terms of TTM revenue.

Tesla looks slightly better on a forward basis, but AMZN and GOOGL seem better deals.

Other Mag 7 peers, except for AAPL, appear more attractive in terms of their EBITDA multiples vs forward growths.

8. Discounted cash flow model provides a reality check

Instead of giving you my base scenario (and getting criticised for not correctly assessing Robotaxi potentials), I will show you what the market is pricing in, at $220 per share.

Today’s Free Cash Flows in $m (stripping out unusual items):

Market-priced-in future Free Cash Flows (check the Y axis).

For the valuation to make sense, the free cash flows need to 35x in the next decade. This requires Tesla to grow at of 30% CAGR and rise to at least 30% EBITDA margin. It CAN happen if the Robotaxi story really unfolds well - 100% growth here, 60% growth there. But it is a demanding feat.

9. Technical analysis

After breaking out of its half-decade-long side-ways action in 2020, TSLA as a stock has traded on sentiment a great deal. This has also been helped by a combination of Tesla’s exponential rise in deliveries during COVID and the stock entering the S&P 500.

While all other six Mag-7 stocks have made new ATHs, TSLA is still at a big 47% drawdown, even after the latest bounce.

Will the recovery last? Or is it post-growth dead cat bounce?

TSLA Daily Chart (Click here to enlarge)

TSLA looks to have bottomed in wave (2) low in April 2024, and now progressing through the heart of micro wave 1 (blue). Completing the even smaller degree wave circle-v to break above $300 would confirm this.

Wave (3) target will be $800, although it could take a while for us to get there.

TSLA Monthly Chart (Click here to enlarge)

On a larger degree, in terms of TSLA’s entire Cycle, Cathie Wood may well be right. Perhaps she is a secret Elliot-Wavist using crazy future fundamentals to create a wave-V matching narrative.

TSLA looks to be progressing through wave circle-5 of III. The Robotaxi development could just be the perfect catalyst for a $1000 share price.

10. To wrap it up

To wrap up TSLA’s investment case in a short paragraph, TSLA looks like it can really take off from the chart technicals, but the fundamentals require more evidence for support.

If TSLA is just an ordinary car company, it should be worth about a quarter of its current valuation, both from a comparable valuation and a discounted cash flow perspective.

But one could try to defend the current price by pointing at the huge opportunity in the FSD/ Robotaxi and Humanoid Robots market, which Tesla may dominate.

Therefore, you could say 75% of the company value (i.e. $500b) is to have a 25% shot at adding $2 trillion in market cap when Tesla does take the crowning spot in Robotaxi, or a 10% shot at adding $5 trillion in market cap for Robotaxi + Humanoid Robots combined. If you think the odds or the payoffs should be higher, then the shares may be worth more.

Finally, in Elon’s own words from the earnings call:

“the value of Tesla overwhelmingly is autonomy. These other things are in the noise relative to autonomy. So I recommend anyone who doesn't believe that Tesla will solve vehicle autonomy should not hold Tesla stock. They should sell their Tesla stock. You should believe Tesla will solve autonomy, you should buy Tesla stock. And all these other questions are in the noise.” - Elon Musk, Q2 2024 Earnings Call

Disclosure: I have a tactical long position in TSLA.

Don't forget - you can claim your 7-day free all-access via my Launch Pass page now!