The Liberated Market, 6 April

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Wait, Wut?

by Alex King, CEO, Cestrian Capital Research, Inc

In our research services we adopt a simple no-personal-politics rule. This has proven very valuable over the years. Of course all our analysts and our subscribers have personal opinions on politics, but everyone leaves those bags at the door. We pride ourselves on being all-business, all the time. To the extent political machinations impact the market, we’re interested and will attempt to interpret and work out the potential range of outcomes. We don’t see the point in hyperbole about whether President X is more akin to Zeus, Hades, or somewhere in between. It’s important to have political views and act on them outside of investing and trading, but it’s counterproductive to allow those views to cross-contaminate investing and trading analysis. Securities prices don’t know anything about politics; they’re just prices. They follow patterns to some degree, even in times of great stress. And understanding pricing and price patterns remains the key to successful investing and trading.

You will have seen in these Market On… notes of late that we’ve sketched out potential bull and bear paths for, eg., the equity indices and those indices remain with in the bull and bear parameters identified. This is unsurprising, since we try to use the methods adopted by large price-setting investors to lay out where markets may move to. So far, whilst you will read all manner of things about seven-sigma events on Thursday and Friday last week, what we have before us is a dramatic form of Flash Crash that followed general weakness in equities. Nothing more, nothing less.

The question is what happens now, and that does depend on political outcomes I think. It’s not unique of us to say that whether the tariff positioning of Wednesday was performative or intended literally is now a primary driver of markets. Either the Administration holds to its position of tariff %ages derived from trade deficit calculations for those countries it chose to include, or it negotiates them lower.

If the Administration meant those tariff percentages literally then we will be in a structural bear market I believe. So the dominant direction would be down, and people would do well to find a way to make money from that. (Unlevered inverse index ETFs are a good risk-adjusted tool for long bear markets in my view. They don’t hurt you too much when violent countertrend rallies come along, but they drift up in value as the market continues to drop lower. For $SPY in bull markets, $SH in bear markets; like $QQQ in a bull, $PSQ in a bear. We use these unlevered long/short pairs in our SignalFlow AI services, of which more below ).

If the Administration means to negotiate then most likely this dip gets bought and we carry on upwards until such time as it transpires whether a move from lower to higher tariffs in the US was a good or a bad idea for the economy. As I have said many times in this note, there’s nothing inherently terrible about raising tariffs a little, and there’s no reason the market can’t eat it up and keep moving upwards. The question is (i) at what level tariffs settle and (ii) the manner in which they settle ie. professional negotiations or chaos monkey methods. Chaos monkey methods can be very effective in and of themselves, it’s just that markets tend to prefer the besuited Wall St. approach. Since I don’t know where the tariff levels will settle - and neither does anyone else - I have no clue whether these tariffs will help or harm the economy and no clue whether in the longer term they help or harm US equities. We just have to wait and see.

Now, an important matter, and the rider is it involves us marketing a subscription service. You’ll forgive me for that I trust. I would ask you to read the testimonials below for our quantitative analysis services. In times of market stress, there is nothing less emotional than a machine. Lines of code don’t have political affiliations and they don’t have preconceived notions of trading relationships between countries. These lines of code don’t even know what the numbers are that they are analyzing. They are just looking for patterns in the numbers. Which is, I think, why our SignalFlow AI services have been (1) so on-the-money of late and (2) so very popular of late. Whether you choose to follow their signals or not, I can tell you that having a completely calm robot buddy on your desk assessing risk is a wonderful thing.

PlungeProtectionTeam.AI

Subscribers to our SignalFlow AI family of services have been very happy of late. Here’s three testimonials we received after the current market turmoil.

- "I am wildly thrilled with SignalFlow AI for $SPY! I have been following the signals and moved almost completely to cash with the most recent change to risk off. Absolutely incredible for me, mentally and financially. Thanks so much to the team for developing this service.” - April 2025

- “The long/short service paid for itself in one day overnight by the way! Thankyou.” - April 2025

- “Rather than a day that could have ruined the weekend, I was able to watch the market tank knowing that I had the knowledge to weather the storm and come out far ahead.” - April 2025

The latest SignalFlow service provides long/short signals for the S&P500 and Nasdaq-100. This is a very easy to use service running on a quantitative model that achieved the following successes in the current market turmoil:

(i) Called “Risk Off” in $QQQ on 28 February this year at the close, with $QQQ at $508. The model remains risk-off in QQQ; since then, QQQ has fallen 17%.

(ii) Called “Risk On” in $PSQ - that’s a 1x inverse QQQ ETF - on Wednesday in post-market trading this week. Since when PSQ is up 8%.

This is pure machine logic driven by price alone, not by the news, not by narrative, not by fear or greed.

Please do take a moment to read about what I believe to be a truly excellent service - here.

Short- And Medium-Term Market Analysis

If you want this daily dose of pattern recognition, and you aren’t yet a subscriber of course, you can read about and choose from all the subscription services that include this note, here.

US 10-Year Yield

On Friday, the 10yr yield hit our Wave 5 target zone and promptly reverse upwards. This is a great example of why using price patterns not real-world analysis is helpful. Tariffs are inflationary. Bonds hate inflation. So if you followed the real world last week, you’d have sold bonds in anticipation of rising inflation. Instead, what I assume was a move to risk-off in equities saw increased appetite for bonds and thus the yield falling sharply in the 10yr.

This pattern suggests the most likely next move, by the way, is for the yield to now rise. If so we will start to measure that next move in the usual way.

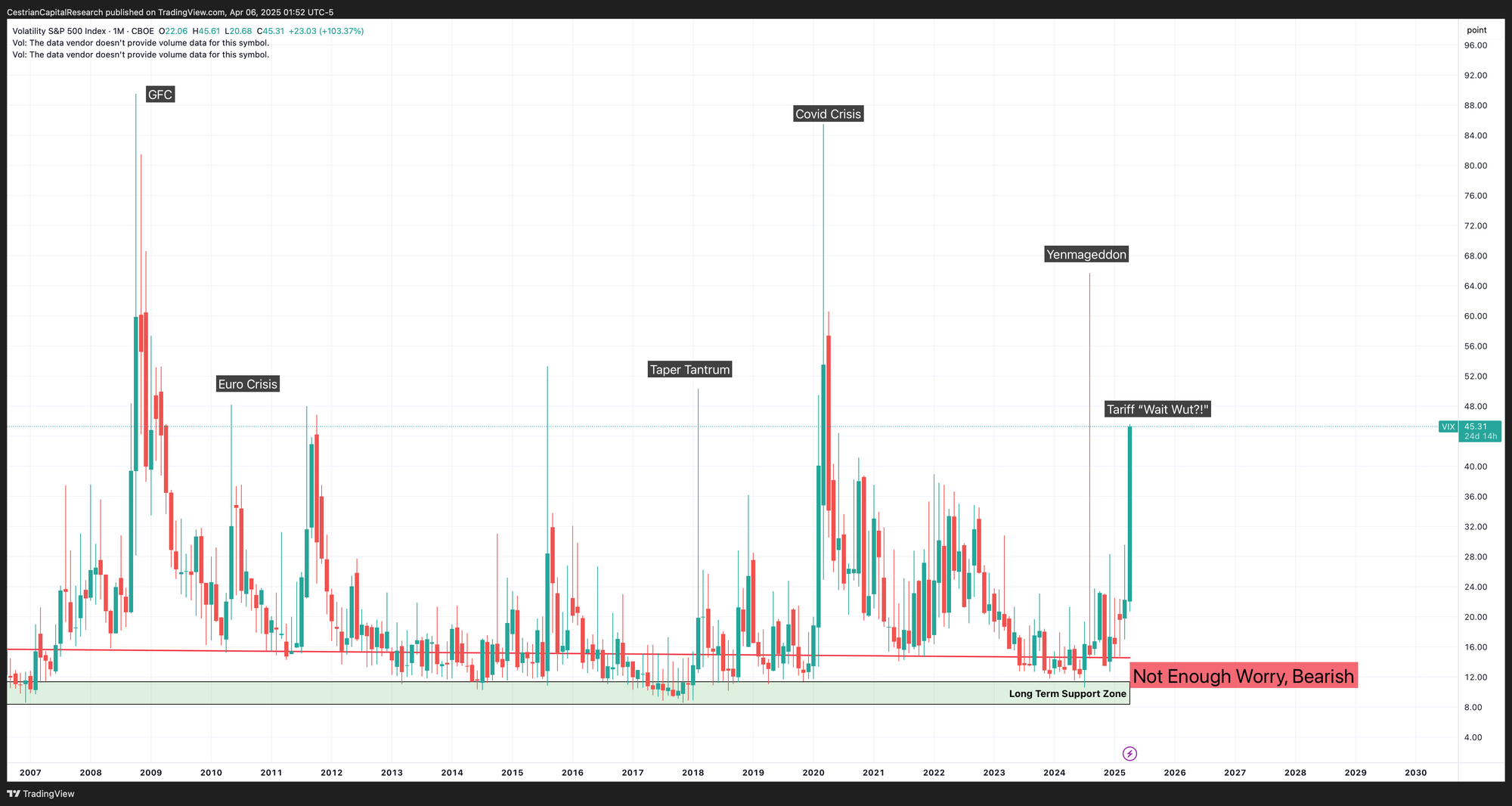

Equity Volatility

Demand for >30 DTE S&P500 puts, monthly chart, 20 year context. Anyone expecting a vol crush on Friday - not a unreasonable expectation - was themselves crushed by China responding in a similar shock & awe manner.

Disclosure: No position in volatility-linked securities.