DataDog Q4 FY12/24 Earnings Review

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

When Consolidation Fails

by Alex King, CEO, Cestrian Capital Research, Inc

Right now there is a veritable wall of point-solution subscription software companies with tradable public tickers. DataDog ($DDOG), Dynatrace ($DT), PagerDuty ($PD), Okta ($OKTA), the list goes on. All of them share a maturing fundamental profile - which in the main means declining rates of revenue growth and rising cashflow margins. All of them have a high rate of recurring revenue, because the thing they do is important to their customers and because replacement costs are high. And many of them trade at bigger cashflow multiples than does Nvidia ($NVDA) despite the fact that they have lower growth rates, poorer cashflow margins, weaker balance sheets and nothing like the structural importance to the market.

Now, typically in software one would expect to see a large consolidator start to mop up these smaller vendors; a Microsoft, an Oracle, an SAP, that sort of large behemoth that long since forgot about innovation of its own. Unfortunately for the point-solution companies and their shareholders, this consolidation has yet to happen. Why? Well, I don’t know, but I suspect it is something to do with the huge rates of capex being incurred by the monoliths as they compete to claim supremacy in AI. If even Microsoft’s balance sheet needs to be corralled and shielded from the worst excesses of build-it-and-they-will-prompt LLM spending, what chance do the smaller whales have? And if all these bigger names have to keep more than a weather eye on their cash reserves, lest they need to buy more GPUs or fund more power generation or whatever it may be, are they going to pay in excess of 50x cashflow for a company which in truth should be no more than a product set for one of these suite vendors? So far the answer is, no.

DataDog has perfectly reasonable fundamentals and the thing it does is no less important to its customers than it was a year ago. I am not aware of any particularly new kid on the block threatening its existence, not least because the available market size to any new systems monitoring vendor just isn’t that big, so it’s not a space likely to attract big VC dollars or new and excitable CEOs. The stock chart looks like it can move up from here. But my question is, does anyone need to own a niche software play growing at 21% pa (that’s the guide for Q1 FY12/25) at a price of 63x TTM unlevered pretax FCF? I don’t think they do. So, personally, I don’t.

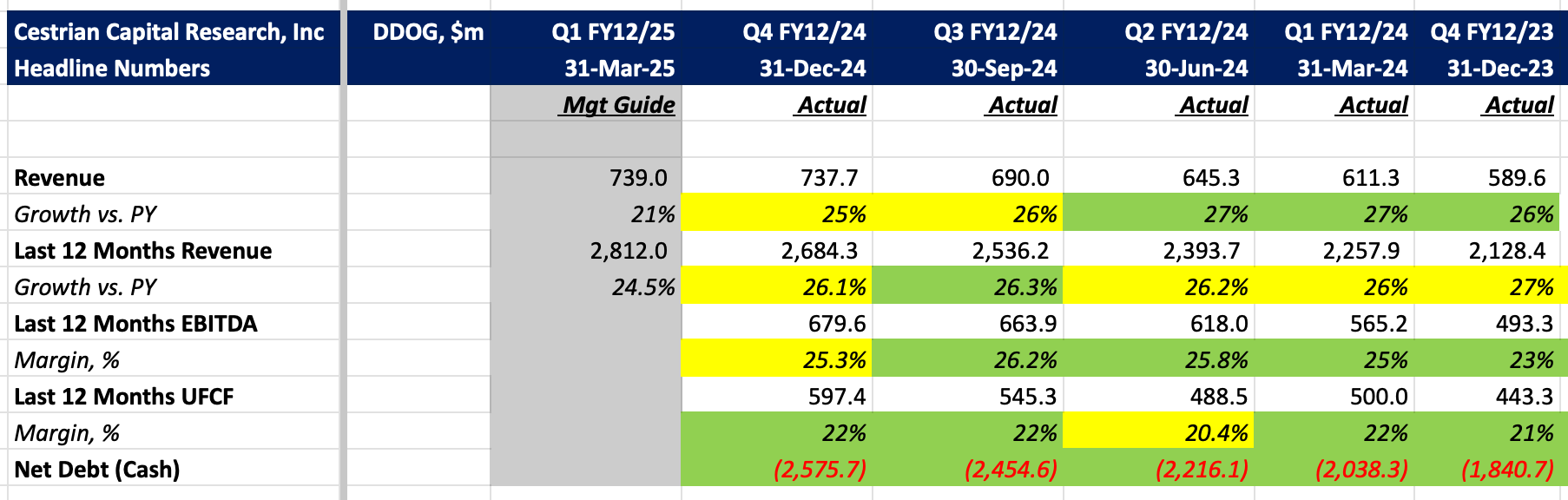

Here’s the headline numbers.

Now let’s get into the detail.